If you want to drill down and see the details of each scenario date per deal.

Select Valuation date.

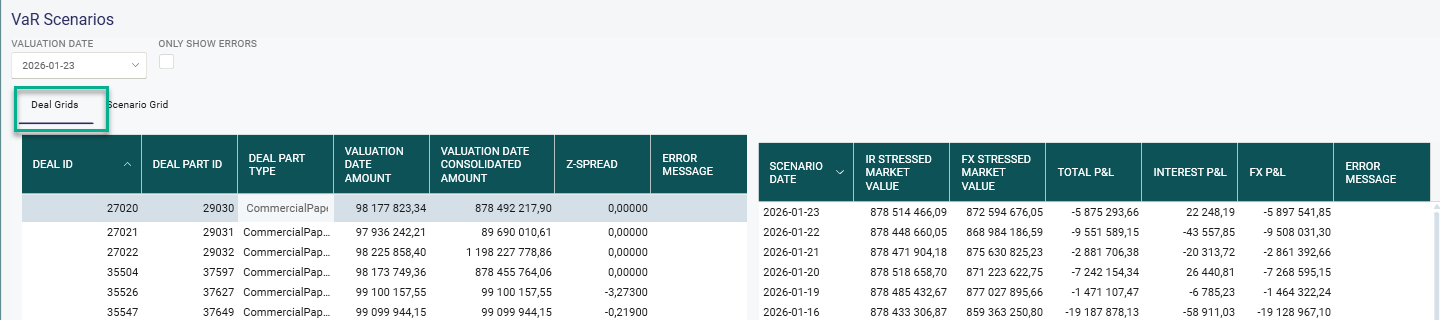

Tab Deal Grid - Shows Scenarios per Deal / Deal part.

Select the deal that you want see details for.

Valuation Date Amount - Market value per valuation date in original currency.

Valuation Date Consolidated Amount - Market value per valuation date consolidated to the currency selected in he System Settings.

Z Spread - Z-spread is calculated for Bonds and Commercial Paper as a fixed spread based on the difference between the Bond price and the Yield curve and is used in the VaR calculation to get a more correct profit and loss value, including the counterparty risk.

Error Message - If Market value is not possible to calculate an error message is shown.

Scenario Date - Maximum 252 days but is decided in the Autopilot run.

Interest Stressed Market Value - Market value stressed with historical changes in interest rate yield curves times FX Rate on the Valuation date.

FX Stressed Market Value - Market value per valuation date in original currency times stressed with historical changes in FX Rates.

Example FX Stressed Market Value

FX Rates - USD/SEK

2026-01-23: 9,50

2026-01-22: 9,40

Difference: 9,50 - 9,40 = 0,10

Calculation of the FX Stressed Market Value on 2026-01-23 = MV * 9,60

Total P&L: Interest P&L plus FX P&L

Interest P&L: Interest Stressed Market Value minus Valuation Date Consolidated Amount

FX P&L: FX Stressed Market Value minus Valuation Date Consolidated Amount

Error Message - If Market value is not possible to calculate for the specific scenario date an error message is shown.

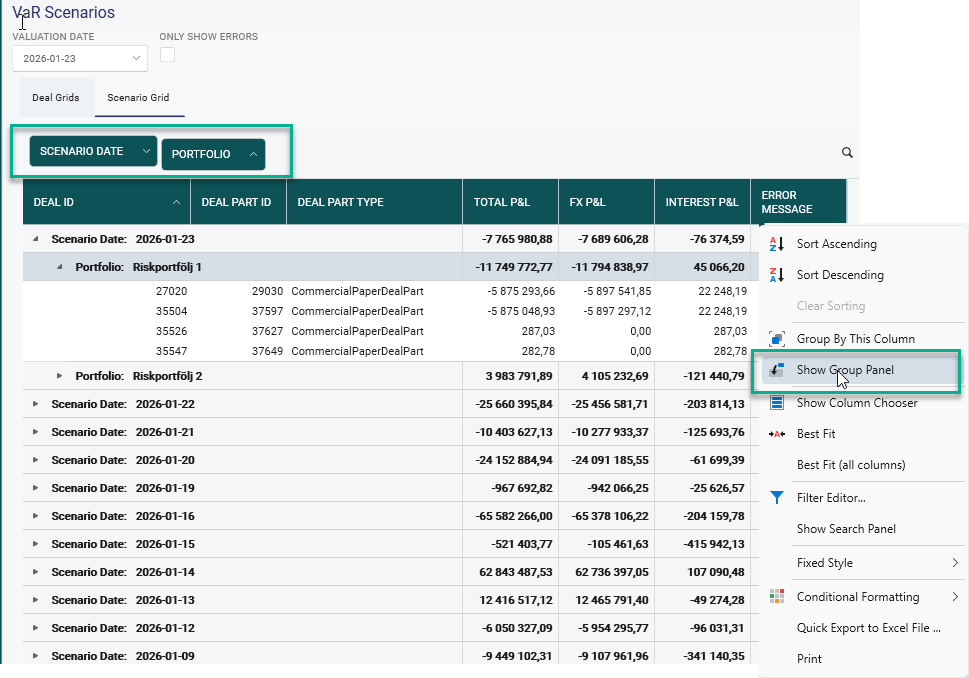

Tab Scenario Grid - Shows all Scenarios. Possible to group by Scenario date, Portfolio, Deal Part type and Deal part ID

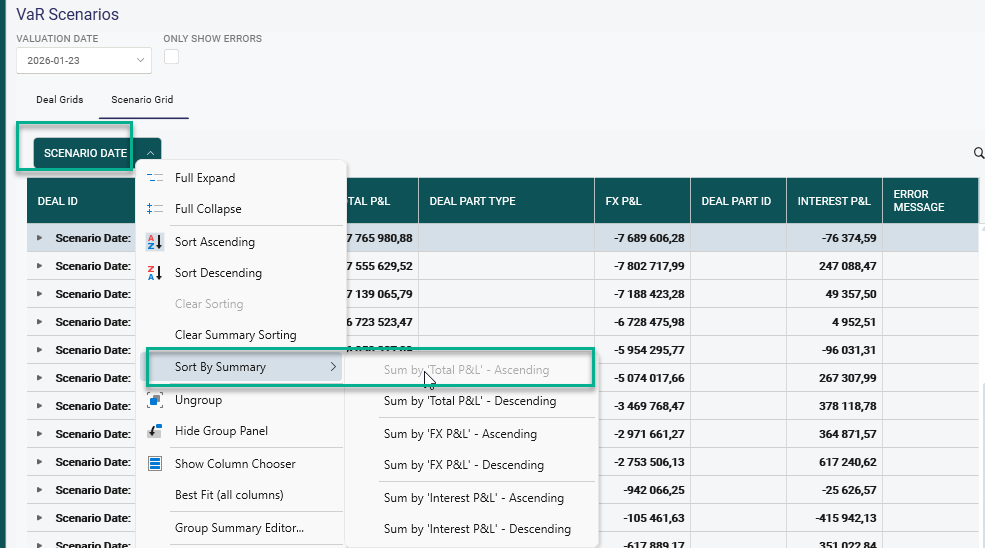

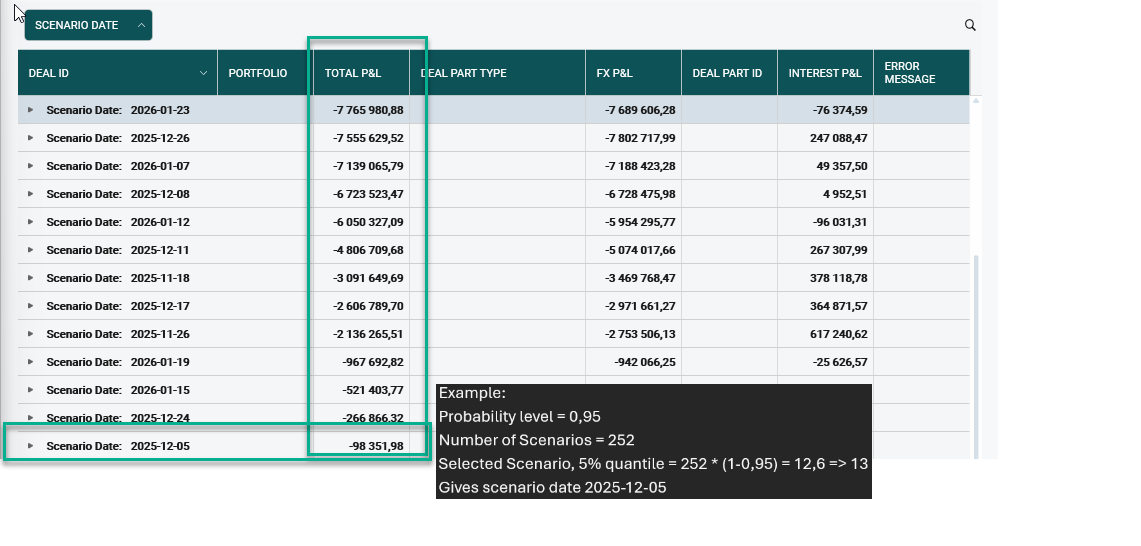

How to find highest Total P&L or Total P&L for a specific quantile.

Right click on Scenario date - Select 'Sort By Summary' and then 'Sum By Total P&L - Ascending'.

Result - Sorted by total P&L per scenario date in Ascending order.

Was this article helpful?

That’s Great!

Thank you for your feedback

Sorry! We couldn't be helpful

Thank you for your feedback

Feedback sent

We appreciate your effort and will try to fix the article